The VEST survey, covering nearly 200 items per vendor, answers that question in glorious detail. You need to examine the report itself to see answers for individual products. But aggregate data provides important context for understanding where the industry stands and where it’s headed.

Let’s start with the basics. I group vendors into three categories depending on their primary customers.

- “micro” vendors sell largely to businesses under $5 million in revenue. These include Infusionsoft, HubSpot, and OfficeAutoPilot.

- “core” vendors sell to B2B companies with $5 to $500 million in revenue. These include LeadFormix, Marketo, Genius,MakesBridge, Act-On Software, Right-On Interactive, SalesFUSION, Net-Results, LeadLife, Pardot, Silverpop, TreeHouse Interactive, Eloqua, Manticore Technology, and eTrigue.

- “enterprise” vendors sell mostly to companies over $500 million revenue. These include Aprimo, Neolane, and Oracle.

As you might expect, products for larger companies have more features available.

(In this and following charts, “feature availability” is the ratio the actual vendor scores to the highest possible scores. The scores are on a scale of 0 to 2, where 0 means a feature is missing, 1 means it is partly available, and 2 means it is fully available. Having a “partly available” option introduces some dangerous wiggle room for aggressive self-scoring, but it doesn’t seem to have been used abused too badly: just 14% of the scores are 1, compared with 21% at 0, and 65% at 2.)

Remember, though: more features is not always better. A feature important to a large enterprise can make a system less suitable for a small company where the feature won’t be used but still adds cost and complexity. The VEST addresses this by providing different weighting schemes for the three types of customers. These weights reflect the most important features for each category and sometimes apply negative values to features that make a system less suitable for the target group. Scores calculated with those weights show that the core and enterprise vendors do about equally well at serving their target markets. The micro vendors have a little more room for improvement.

Speaking of improvement, we can also see how the industry has changed by comparing the new VEST with scores from one year ago. This brings considerable good news: the micro and core vendors are indeed adding features, especially in lead generation, campaign management, and reporting. Enterprise systems are already so powerful that new features don’t matter much.

(The decline in “scoring and distribution” for the enterprise category is a bit of a fluke: one vendor was replaced by another with weaker scoring and distribution features. Because there are only three vendors in the group, this has a large impact on the total.).

The change in weighted scores shows roughly the same story – so, for the most part, vendors are adding features that matter.

But enough generalities. What really matters is specific features. Today I’ll look at the areas of greatest improvement. A later post will list key features that remain hard to find.

I’ll focus on the core vendors, since those are the systems that most B2B marketers will purchase. Each chart below has three columns:

- “change”: the change in feature availability among core vendors, compared with the January 2011 VEST.

- “core”: the feature availability for core vendors in the January 2012 VEST

- “enterprise”: the feature availability for enterprise vendors in the January 2012 VEST.

Let’s start with three areas that gained a lot of industry attention last year: Webinars, social media, and revenue management.

Webinar Integration: Webinars are an increasingly important marketing tool, but traditionally systems like Webex had their own registration forms and result tracking. Moving the information into marketing automation required time-consuming file extractions and imports. Last year, the Webinar vendors began to expose APIs to allow automated integration with the marketing automation systems, and the marketing automation vendors leapt on the opportunity. As a result, availability of Webinar integration grew rapidly. This is a rare area where the core vendors outscore the enterprise vendors, perhaps because the enterprise vendors are less narrowly focused on B2B needs and/or because they tend to move more slowly at enhancing their products.

Social Media: It’s no news that social media is a hot topic among marketers, so it’s no surprise that vendors are adding features to support it. But even after last year’s improvements, anything beyond basic sharing and tracking remains hard to find. This is another area where the enterprise vendors are lagging. For a more nuanced analysis, see my blog post Social Media Features in Marketing Automation Systems: Who Does What? from last December.

Revenue Management: We heard plenty last year from marketing automation vendors about revenue management. The good news is that they’ve backed up their words with features. In fact, it’s surprising how widely many key revenue management requirements are available – many industry leaders can walk this walk, even though a few do most of the talking. Note also that the enterprise vendors do most of this as a matter of course.

Okay, those were interesting but expected. What else were vendors working on last year? Several things, it turns out.

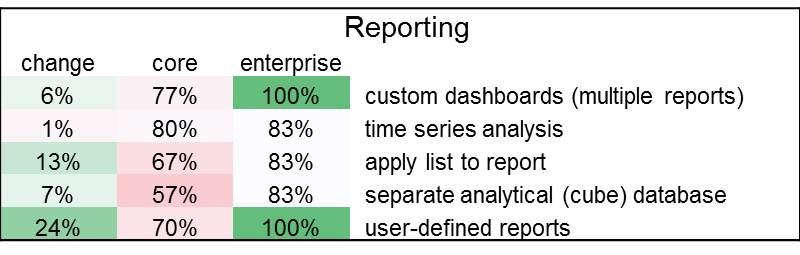

Reporting: Enterprise vendors have long had better reporting than the core marketing automation systems. They still do but the gap is closing. A separate analytical database is especially important for advanced analytics in general and for revenue management reports in particular. Again, it’s more widely available than you might think.

Dynamic Content: This refers to embedding content selection rules within an email, Web form, or landing page. It’s not just personalization, which simply plucks information from a database field, and it’s not segmentation, which uses rules to select different content objects within the campaign flow. Dynamic content lets one email or Web form serve different segments, so marketers don’t have to create and keep track of so many separate versions. As you’d expect, it was traditionally used in enterprise systems where complexity is a more pressing challenge. Core marketing automation vendors didn’t talk about it much last year, but quite a few seem to have added it.

Cross-Campaign Coordination: This encompasses several features to help coordinate customer treatments across campaigns. As with dynamic content, these become important when companies are running complicated marketing programs and need to keep things under control. It’s another area where core marketing automation systems are closing the gap with enterprise vendors, although some distance still remains.

Lead Scoring: remember that old Sesame Street song, “One of these things is not like the others”? You wouldn’t expect lead scoring on a list of most-improved marketing automation features, since it’s been a key marketing automation capability all along. But last year did see substantial rise in systems that provide multiple scores per lead, and a smaller rise in the ability to recalculate leads on a schedule (as opposed to when a trigger event occurs). Both are markers of advanced systems. We may see lead scoring on next year’s most-improved list too: plenty of vendors still lack other advanced lead scoring features. (If you’re wondering about the negative changes, they happened because several new vendors entered the core group with limited scoring features.)

So that's the good news: changes in areas the vendors talked about plus some changes they didn't necessarily trumpet. Look for my next post to learn where they still need to strengthen their products.

Of course, the only thing more exciting than reading my analysis is to make your own. For more information about the VEST report or to order your own copy, visit the RaabGuide Web site.

0 comments:

Post a Comment